Ukraine Khmelnytskiy Oblast 2019

1. The main purpose of the 2019 PEFA assessment is to provide the Government of Ukraine with an objective and up-to-date diagnostic of the public financial management performance at the oblast level of subnational government based on the latest internationally recognized PEFA methodology. The 2019 PEFA is an assessment of the quality of the Ukrainian PFM system at the subnational level of and monitors the results achieved through PFM reforms undertaken since the 2015 central government PEFA assessment. More specifically, the PEFA assessment measures which processes and institutions contribute to the achievement of desirable budget outcomes, aggregate fiscal discipline, strategic allocation of resources, and efficient service delivery. The Ministry of Finance of Ukraine has expressed its interest to update the 2017-2020 PFM Reform Strategy based on 2019 PEFA’s findings and subsequent recommendations.

2. This assessment covers the Khmelnytskyi oblast administration which consists of 17 budgetary institutions. Where relevant it covered national bodies that are responsible for certain activities in the oblast: State Treasury; Authorized Body for Procurement Service (Ministry for Development of Economy, Trade and Agriculture), State Audit Service, Accounting Chamber, and State Fiscal Service. It also covered the Budget Committee of the oblast council.

3. The PEFA assessment was undertaken by the World Bank under the Parallel EC-World Bank partnership Program for ECA Programmatic Single-Donor Trust Fund/EU Program for the Reform of Public Administration and Finances (EURoPAF). The assessment oversight and management team include the Ministry of Finance of Ukraine, the World Bank, and the Delegation of the European Union to Ukraine as well as representatives from the oblast administration. The assessment covered fiscal years 2016 to 2018 and was performed in August/September 2019. The cut-off date was September 30, 2019. Assessment management and quality assurance arrangements are presented in Box 1.1 below.

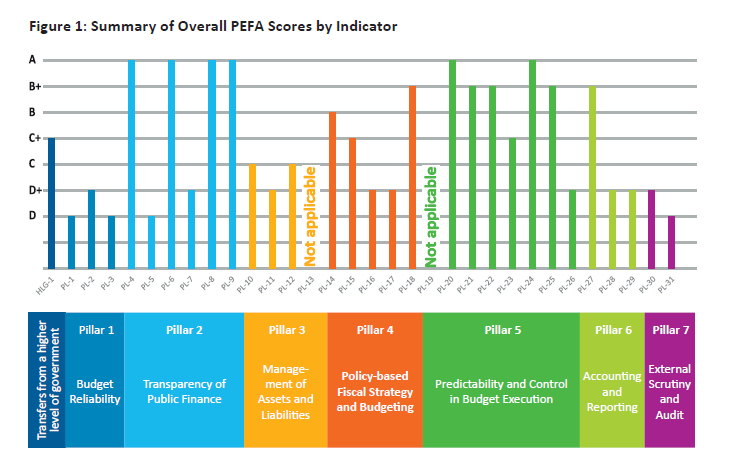

4. The challenges in producing accurate total revenue projections have not been met in recent years. Actual revenues were significantly greater than estimates and grants from the central government were also greater, apart from in 2018. Actual total revenues from all sources were much higher than estimated in the planned budget. As a result, the aggregate expenditure side of the budget has not performed well, and budget execution required the use of virement and two supplementary budgets both following the Budget Code.

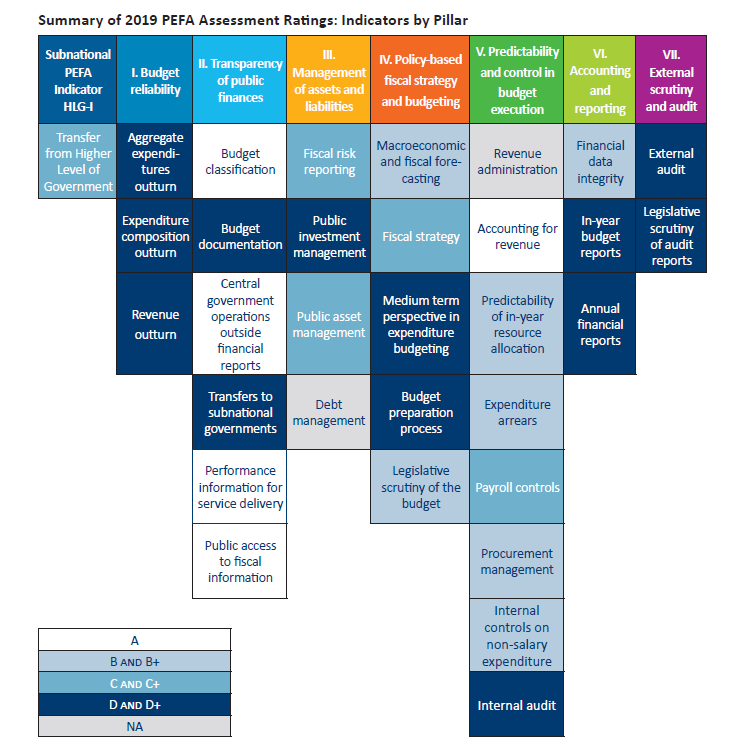

5. Ukraine, both at the central and subnational levels of government has an impressive array of information regarding the finances of budgetary government, but transfers from the oblast to lower level governments which are financed by the oblast’s own budget sources lack a rule-based approach. The Chart of Accounts, which underpins budget preparation, execution and reporting, is comprehensive and consistent with Government Financial Statistics (GFS) standards. Information is included in the budget on a timely basis. The largest proportion of transfers to subnational government is channeled through the oblast from the state budget transfers. Those transfers are determined by and financed from the central government, and therefore they are not subject of this assessment. Out of the entire amount of transfers assessed in the relevant indicator, 45.5 percent were allocated without transparent formula based approach. Lower level governments reported within nine months after the end of the budget year. Information on performance plans and achievements in service delivery outputs and outcomes in the oblast is good and is based on the program budgeting system with performance plans, performance achieved and performance evaluation reflecting the “program budget passport” system and the work of the Balance Commission in its evaluation. Tracking of resources to service delivery units reflects the strong accounting. Public access to fiscal information is strong. There is a citizen’s (summary) budget available.

6. A comprehensive and inclusive process is lacking in public investment management. Economic analysis is not carried out for the major investment project, and project costing and project monitoring do not meet the basic requirements. Despite this, the process for the selection of investments is nevertheless good reflecting the interagency commission and its standard criteria for choosing projects. Information on the disposal of assets included into the budget reporting is weak. The oblast has no debt as of the time of the assessment.

7. Some progress has been made towards a comprehensive medium-term expenditure framework.There is good information on the specification and evaluation of key performance indicators. A mediumterm approach is taken to key spending units’ (KSU) budget proposals but not to the formulation of annual budgets. The adopted overall fiscal strategy focuses on the budget year and does not examines changes from previous forecasts but there is reporting against fiscal outcomes in the budget execution report. There are no hard ceilings for budget preparation and the budget program proposals are used for annual budget estimates only. There is a budget calendar, and it provides spending units less than four weeks to prepare their budgets. The legislature gets less than one month to carry out its scrutiny function, but it approves the budget on time. Nevertheless, the oblast legislature only considers aggregates for the upcoming budget year and not the medium-term. The procedures and timetable for budget scrutiny are respected.

8. The State Fiscal Service of Ukraine is responsible for revenue collection at the time of the assessment on behalf of the oblast. Revenue collected is well managed in terms of the flow of funds to the Treasury and recording of transactions that are collected on behalf of the oblast. All revenues are paid into the oblast account with the Treasury. All accounts are reconciled on a timely basis. The State Fiscal Service can monitor revenues in real time. Payments to the Treasury Single Account are reconciled on the 4th day of each month. A revenue report is prepared monthly for management purposes.

9. The consolidation of cash balances in the Treasury Single Account (TSA) at the National Bank of Ukraine is made daily. The Finance Department forecasts the annual cash flow broken down by month but only updates it periodically. Spending units know their annual budget within one month of approval of the oblast budget and can commit funds up to the value of their annual budget allocations and make payments up to the value of their monthly apportionment limits. Management of budget releases using strong commitment control processes has been successful in managing arrears.

10. Each department is responsible for maintaining its own payroll accounting system. Information on employees, which is accounted for by the human resource unit, and remuneration processed by the accounting department, is reconciled. Changes to the employee information and on salary are made within three months. Budgetary institutions have clear and detailed rules and procedures for making changes to staff and payroll information. These include the requirement for signatures of authorized persons and provide a clear audit trail. The State Audit Service monitors the eligibility, timeliness and completeness of salary payments based on regular inspections

11. The public procurement system is strong. This reflects the national ProZorro electronic procurement platform which the oblast uses. It has been recognized internationally and has received several awards. However, in the oblast only 65 per cent of purchases were carried out by competitive methods.

12. Internal controls on non-salary expenditure are positive. There are effective commitmentcontrols and compliance with payment rules and procedures. Improved segregation of duties with clear responsibilities is ensured by the “E-Treasury” management information system that supports the TSA. The internal audit function is split between the oblasts’ small internal audit unit and the Western Directorate of the State Audit Service. Internal audit activities are primarily focused on compliance with some assessment of efficiency. Internal audit activities are guided by Ukrainian Internal Audit Standards. The implementation of internal audit recommendations ensures its effectiveness and the recommendations are implemented in an appropriate time period.

13. Accounts reconciliation and financial data integrity are areas of strength. The bank reconciliation for the TSA takes place daily. There are no suspense accounts. Generally, advance accounts are reconciled monthly based on reporting by spending units. Data integrity is good as access and changes to records are restricted and recorded, thereby producing a sufficient audit trail. However, the system lacks a dedicated operational unit.

14. With respect to in-year budget reports, coverage and classification in reports allows partial direct comparison to the original budget. Treasury’s reports on expenditure are based on economic and functional classifications, but not on administrative classification. This does not allow comprehensive direct comparison with the original budget. Information includes all budget estimates for the spending units. There are both monthly and quarterly budget execution reports that are issued within 15 days from the end of month and within 35 days from the end of the quarter. Initially, basic information is provided monthly with detailed follow up information quarterly. There are no material concerns regarding data accuracy. Information on expenditure is provided at the payment stage (only unpaid commitments are shown). The oblast state administration (OSA) prepares additional quarterly reports based on the administrative classification but they are not presented in the same format as the original budget.

15. The financial statements include complete information on assets, liabilities, including long-term,revenue, and a reconciled cash statement. Treasury’s reports on expenditure are based on economic and functional classifications, but not on administrative classification, which does not allow for their direct comparison with the original budget. The financial statements are produced within three months after the end of the reporting year but have never been submitted for external audit. The national public sector accounting regulations that apply to all financial statements are largely consistent with the international standards. Notes to the financial statements clearly disclose the accounting framework and standards used in preparing annual financial reports. However, the differences between applicable national provisionsand IPSAS are not presented. The OSA prepares additional annual reports based on the administrative classification but they do not follow the form of original budget.

16. An external audit at the oblast level is not routinely carried out. As a result, legislative scrutiny of audit reports does not take place. The finacial statements are reviewed by the oblast council.

17. The internal control environment is generally sound. The controls associated with the day-to-day transaction of the oblast budget are functioning and result in good data integrity regarding the activities of these entities. The laws and regulations provide the legal framework, and allow for specific roles and responsibilities, segregation of duties, and operating processes. The system embeds access controls and audit trails that support the internal control framework. The budget execution reporting system that provides information on performance relating to service delivery enhances the overall control environment. The oblast’s Balance Commission reviews expenditure performance in relation to service delivery and provides independent evaluation and makes recommendations on service delivery performance, however results of those reviews were not published regularly.

Aggregate Fiscal Discipline

18. While revenue administration ensures that revenues are efficiently collected, the relative weaknesses in forecasting both own revenue and the transfers from the central government have undermined overall fiscal discipline. Nevertheless, implementing the planned budget, on an aggregate basis, to accommodate unplanned revenues is assisted using virement and supplementary budgets following the procedures laid out in the Budget Code. Treasury operations and cash management enables expenditures to be managed within the available resources as they become available. Control of contractual commitments is effective and has removed expenditure arrears. The absence of a full external audit function may inhibit fiscal discipline, but the operations of the State Audit Services go some way to partially replace it.

Strategic allocation of resources

19. The Chart of Accounts caters to a multi-dimensional analysis of expenditure. The provision of budget information to citizens makes them aware of what is being spent and encourages them to demand resources to be directed to their needs. Despite the fact that oblast budgets are adopted annually and the program proposals are used for annual budget estimates only, there is a medium-term perspective in expenditure budgeting at the level of key spending units. Performance indicators are specified, and there is assessment of and independent evaluation of performance achievement. The work of the oblast’s Balance Commission provides a critical review of performance. There is an emphasis on overall fiscal forecasting but this does not extend to a multi-year fiscal strategy to assist in resource allocation.

Efficient use of resources for service delivery

20. While reconciliation between payroll and personnel records is in place, they are not fully integrated. The strengths in the accountability mechanisms provide counter-checks on inefficient use of resources although regular external audits of full annual financial statements are still needed. In-year and annual budget execution reports are not fully comparable with the form of original budget. Publishing of performance targets and outcomes supports the efficient use of resources in service delivery units. The reviews of expenditure performance by the Balance Commission are a positive feature of the oblast’s PFM system.t as it was not legally allowed to borrow.