Cambodia Phnom Penh 2022

Executive Summary

This subnational PEFA performance assessment for PPCA is conducted under the direction of the Steering Committee of Public Financial Management Reform (PFMR-SC), with coordination and implementation by the General Secretariat of Public Financial Management Reform Steering Committee (GSC) and technical support from the IMF.

The PFMR-SC issued a decision no.080 MEF dated 02 September 2019 on establishing a Working Group for PEFA Performance Assessment for PPCA. This working group consists of members from MEF (GSC, GDNT, GDB, GDP, GDT, GDSNAF, GDPP, GDSPNR, and GDIA), MOI, MoH, MoEYS, NAA, NCDD, MCS and PPCA with the following roles and responsibilities as follows:

• assess PEFA performance of PPCA and submit this performance report to the PFM Reform Steering Committee for approval;

• prepare a PFM reform action plan for PPCA based on findings from the PEFA performance assessment of PPCA report;

• use findings from the assessment as inputs for the preparation of CAP4 of PFMRP to modernize the SNA budget system.

To ensure this subnational PEFA performance assessment report for PPCA’s quality, an essential peer review process is provided through consultations and document review by a range of development partners, including the EU, WB, ADB and UNICEF, in addition to circulation across the MEF stakeholders and the PPCA for review.

Rationale and purpose

The timing for this PEFA assessment for subnational PFM system targeting the PPCA also comes at a critical juncture for the PFM reform agenda at both the national and subnational levels. More specifically, at the national level, the platform-based PFMRP is currently in its final year of the designated horizon for Platform 3 by extending for two years, with work already underway on formulating the CAP4 expected to cover the period 2023-2027. Findings from this subnational PEFA assessment report for PPCA, together with the national PEFA performance, are important contributions to the formulation of CAP4 objectives across a range of PFM component-level objectives, including those pertaining to budget preparation, budget execution, budget control, and financial performance report, as well as for the CAP4 objective specifically targeting subnational financial management and fiscal decentralization issues.

As noted above, this subnational PEFA performance assessment for PPCA focuses on PFM performance, systems and processes of the PPCA. The decision to specifically target PPCA reflects two key considerations. Firstly, Phnom Penh is not only the capital and the largest city in terms of population, but it also has a uniquely dominant status in terms of economic, business activities and public finance management. Finally, Phnom Penh as the singular focus for this subnational PEFA performance assessment for PPCA allows for the capture of a large proportion of total subnational public financial activity, including both revenue and expenditure.

This report presents significant findings of the first assessment of PFM systems in the PPCA applying the SNG PEFA methodology. The results of the assessment will be used as an input for the preparation of the PFMRP CAP4 for Platform 4 covering the period 2023-2027. More generally, this exercise assists the RGC to understand more clearly key elements of the overall PFM system.

The results of this assessment cannot be applied for other provincial administrations since the Phnom Penh has a unique status within the scope of SNAs, implying some limitations on the direct comparability of findings for provincial administrations. However, it becomes a baseline for the next assessment as well as improving the PFM system.

Coverage of assessment: The assessment covers the PPCA, its executive, spending units and council, the services supplied under its authority, as well as PFM activities involving interaction with the central government. There are no extra-budgetary units or public enterprises under direct supervision of PPCA. The assessment uses data for the 3-year period (2018, 2019 and 2020) for many indicators, while also referring to processes and/or data for 2021, as required by specific performance indicators.

Main strengths and weaknesses

The main findings of the subnational PEFA performance assessment are focused on whether the PPCA has appropriated systems in place to support achieving the three main fiscal outcomes, namely aggregate fiscal discipline, strategic allocation of resources and efficiency in the use of resources for service delivery or not.

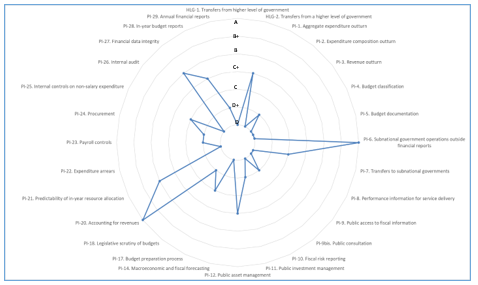

The assessment results show that the PPCA’s PFM system is still in the early stage of development, certainly needs more time to improve. In fact, 4 of the 34 indicators score either “A” or “B”, for a performance considered above the basic alignment with good practice; 6 indicators score “C” or “C+” that suggests basic alignment with the international PFM standards, and 18 indicators scored “D” or “D+” that suggest weak performance, 3 indicators are ‘NA’ (PI-13, PI-19, and PI-31) and 3 indicators are ‘NU’ (PI-15, PI-16, and PI-30) as indicated under diagram 01.

Diagram 0.1: Summary score of PPCA’s PFM system

- Strengths

The PPCA depends on its own source revenue and tax revenue sharing; ordinary annual budget preparation is submitted to the MEF on time to consolidate to Council of Ministers and Parliament, and most of the key elements of PFM system are existed. The sound PFM system is required strengthening institutions, regulatory frameworks, and capacity development.

- Weaknesses

The weaknesses of PPCA’s PFM system are found such as (1) limited coordination for budget preparation, (2) limited check and balance mechanism between executive branch and councils since the PPCC lacks technical support to review and scrutinize the medium-term budget expenditure, annual budget plan and execution as well as audit report, (3) limited transparency due to lack of publishing the budget document to public and public participation in the budget cycle, (4) lack of using competitive public procurement method. This competitive method is to ensure the value of money, economy and accountability, (5) lack of monitoring and evaluation performance mechanism and internal arrangement to ensure that public service delivery plan is set by program and sub-program, (6) lack of financial skills to provide technical support to match with the speed of reform, (7) limited BSP and PB quality due to not clearly identify outputs, outcomes, and targets in the program/sub-program, and (8) lack of predictable budget execution. These weaknesses indicate the deficiency of system to be effective management of policy and program, budget management and internal control ensures that policies, regulations, and laws are complied with during the process of budget execution.

Addressing the PPCA’s PFM system gap is to support to implement the new budget system, known as performance budgeting, by 2025. The performance budgeting system can only be successful if every spending agency can explicitly define the outcomes which services (outputs) aim to deliver.

Impact of budgetary and fiscal outcomes

- Aggregate fiscal discipline

Overall, fiscal discipline is still a matter of concern for both spending and revenue collection since it is not realistic and implemented as passed. Transfers from a higher level of government (HLG-1, rated ‘D+’) and fiscal rule and monitoring of fiscal position (HLG-2, rated ‘C+’). The expenditure outturn indicated weak performance (PI-1, rated ‘D’ and PI-2, rated ‘D+’); expenditure arrears are still challenged by a lack of proper definition for arrears aligned to the international standards, lack of an effective expenditure monitoring process (PI-22, rated ‘D*’), and lack of monitoring on lower SNAs (PI-10, rated ‘D’).

Revenue outturn (PI-3, rated ‘D’) remains a big deviation that needs to strengthen revenue forecasting. One of the fundamental issues with revenue from state property is the limitation of state property registration and inventory management due to a lack of information technology systems.

The PPCA prepares and monitors its budget based only on economic classification. The budget documents include economic classification (PI-4, rated ‘D’) and quality of performance and structure of program needs to improve more because PPCA’s BSP preparation is not effectively integrating the SNA’s plans, including aligning PPCA specialized line department’s BSP. Nor does the PPCA’s BSP clearly define expected outcomes and outputs (PI-8, rated ‘D’).

The public investment management (PIM) is still in early-stage (PI-11, rated ‘D’) and asset management needs further improvement (PI-12, rated ‘C+’). Internal control on non-salary expenditure is partially effective but the effectiveness of expenditure controls and compliance with payment rules and procedures can still be improved (PI-25, rated ‘C’).

- Strategic allocation of resources

The weaknesses still persist with the lack of comprehensiveness of the budget documentation, and its classification (PI-5 rated ‘D’ and PI-4 rated ‘D’) and lack of reliable and timely information provided on the transfers to PPCA, khans and sangkats, which prepare their own budgets (PI-7, rated ‘C’). Transparency to the public is limited due to lack of publication of fiscal information (PI-9, rated ‘D’) and public participation in the budget cycle (PI-9bis, rated ‘D+’).

Timing for BSP preparation is very important for PPCA to have enough time to consolidate and make it align with NSDP, 5-year Development Plan, PIP and line departments’ BSP. Additionally, the quality of BSP including program structures and KPIs for outputs and outcomes is weak due to not being clearly defined and provided good quality for measuring performance (PI-14, rated ‘D’).

The PPCC reviews mainly on details of revenue and expenditure included in the budget proposals but lacks discussion policies and medium-term budget expenditure (PI-18, rated ‘D+’ and PI-31, rated ‘NA’).

- Efficiency in use of resources for service delivery

The medium level of predictability in funds available to the PPCA during budget execution (PI-21.2, rated ‘B’) and to khans (PI-7.2, rated ‘C’) support efficient service delivery. The performance monitoring and evaluation systems for service delivery have to be developed for the PPCA (PI-8.4, rated ‘D’) and linked with basic performance of public asset management (PI-12, rated ‘C+’). The PPCC scrutinizes medium-term budget expenditure (PI-16.3, rated ‘D’) that faces challenges due to the extremely short period allowed in practice for this process and technical support to ensure the check and balance mechanism in place.

The value of all contracts awarded through competitive methods in the last completed fiscal year accounted for 10% of the total value of all contracts, meaning a large majority of procurement is conducted using non-competitive methods about 90% (PI-24, rated ‘D+’). Combined with the expenditure arrears control (PI-22, rated ‘D*’) is unlikely to generate good value for money on subnational expenditure.

Deficiencies in the internal control systems (PI-23.4, rated ‘D’; PI-25.2 rated ‘C’ and PI-25.3, rated ‘C’ and PI-26, rated ‘D’) despite timely and orderly reviews by the legislature (PI-31, rated ‘NA’) and low extent of public transparency (PI-9, rated ‘D’; PI-9bis, rated ‘D+’) to limited of efficiency in the use of public resources.

Overall, the subnational PEFA performance assessment for PPCA confirms that there is a need to further strengthen the PFM reforms in the PPCA in order to establish a solid foundation for improving PFM system as well as supporting D&D reform journey.